Did you know that according to the Bangko Sentral ng Pilipinas’ 2019 Financial Inclusion Survey, only 53% of the adult population saves?

This result is as alarming as it sounds. That’s why awareness on the importance of saving money should be discussed more.

World Savings Day is a dedicated time frame where financial institutions whether public or private including financial advocates can gather and promote saving mobilization. The idea is clear – saving is for every Juan!

Saving is the process of putting cash/money and parking it in a safe place and can be accessed easily when needed.

Here are more reasons why you should know how to save money:

- To reach financial independence

The ultimate goal to those personal finance savvy is to finally reach total financial independence wherein you never have to worry what tomorrow will bring in terms of your finances. This can only be achieved if you take care of your money.

- To be prepared in case of emergencies

Unexpected expenses such as car repair, loss of job, medical issues in the family call for an emergency fund. Your savings could cover the amount needed for the said unexpected expenses so you won’t be in debt.

- To reach a financial and/or personal milestone

Saving money enables you to achieve each of the financial and personal milestones you may have.

Without proper savings you can never buy and invest for a house and lot or a start up business for example. You need to save money to have enough down payment on a bigger house. Other personal milestones include a new car or a trip abroad etc.

- To not pass up an opportunity

Sometimes life opens opportunities to us that can cost money. Opportunity like a seat sale to your dream destination, a pre-sale house and lot within your budget, a new stock on its IPO stage or even a new business idea.

Your savings can be your starting capital. Remember, the more money you have, the more options you’ll be getting.

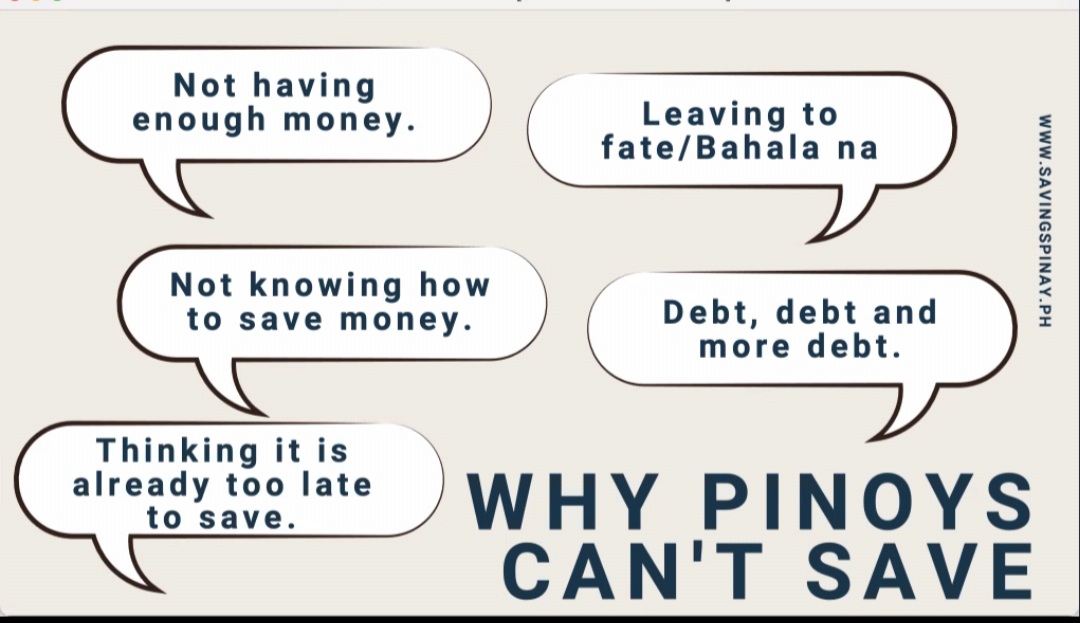

According to most Filipinos, they find it hard to save money because of not having enough money. Leaving things to fate a.k.a. bahala na mentality. Not knowing how to save money. Debt, debt and more debt and thinking it is already too late to save.

And here’s what we need to remember: Saving money is the single most effective way to get rich. If you can live within your means, save and invest the rest, you have done well for your future self.

One of the biggest financial lessons this current pandemic situation has taught us is how important saving money is. Emergencies do happen and those without any money prepared, will find themselves worrying how to put ends meet.

The pandemic also opened new found time for people to do their side hustles for extra income. From people becoming bakers, online sellers, or vloggers, to businesses in line of health supplies like masks booming.

This can also be an opportune time to sell any unused items you have once you do a general home cleaning. Lastly, school transitioning to online also means extra savings for lunch and commuting, same with those who are working in the office.

We were always taught that saving money each month is important but we weren’t aware of how much we should really be saving. Of course not all of our income can be put in our reserve money.

It all depends on certain circumstance below: Your Age, your idea of perfect savings depends on your age.

People in their 20’s will have plenty of time to worry about their retirement so most of their saving goals are short-term. They may be thinking of a car, a condo, a gadget or a branded handbag. Thus, how much you save each will be lower.

Once you hit your 30’s your priorities will differ.

You start to build a family of your own and will have to take care of your aging parents too. Your savings will be long-term now. You start to think about retirement, your kids’ education and your health.

This will require a bigger amount to save each month. Your age surely plays a vital role in knowing how much you should save.

- Your Goal

Goals are just a permanent part of every financial move a person should do. They are the reason why you are doing the things you do.

Short-Term Goals are things achievable in less than a year. This could be the vacation abroad you’ve always wanted, a special gift to your loved ones or a debt you’ve wanted to pay off.

Mid-Term Goals are things that are achievable in 5-10 years time. This could be a house, payment for your wedding and/or start a business.

Long-Term Goals are the ultimate things you want to achieve. Retirement is a solid example of a long-term goal you want to think deeply about.

Have you listed your goals yet? Once you manage to specify your objectives you will be surprised at how quick you are in coming up with the next actions.

- Your Income

Your income has a lot to do with how much you’ll be able to save.

Maybe you are thinking of a saving goal that’s too much that what you’re being paid. If you want a better savings you need to increase your income, find other sources of extra money you can put in your kaban.

Given the three circumstances above, this is how we will approach the whole “How Much Should I Save” question: Save according to your span, your reach and your means.

The more your income grows, the more your savings you should have and not the other way around. Treat it as a never-ending cycle of wealth.

How do you save more money?

- Review your finances. Make sure that you have an idea of your current financial situation. One way you can do this is by calculating your net worth. It is essentially the difference between your total assets minus your total liabilities.

- Make a budget. A budget is an estimate of your income and expenses over a set period of time. Normally done on a monthly basis, budgets work to:

Allocate your salary/income/money wisely

Know how much is coming in and going out in your cash flow

Identify the areas where you can spend less to save more

If you don’t have a budget, now is the time to create one. And if you are already budgeting, it’s best to take a look at how you budget your money and keep it as effective as possible.

- Track your spending. This is one of the most overlooked ways to save money especially but, super effective – track your spending. Record where your money goes and match it with your prepared budget.

- Cut back on unnecessary expenses. Take a look at your recurring expenses and see where you can cut down. Is there a particular subscription you can omit? Can you adjust your utility bills and find ways on how to conserve your water or electricity.

With more people stuck at home it’s easy for our utility expenses to go high. Make sure that you talk with the people in the household and share to them your goal to save as well. Through proper communication, everyone will get involved and it’s way easier to achieve your objective to save more money.

- Learn to live within your means. Living within your means doesn’t mean limiting yourself. To live within your means is simply making necessary adjustments to maximize the limited money/asset you have.

- Set saving goals. Set your yearly and monthly financial goals now. Goals work as motivational tools that will keep you from building wealth instead of the other way around. Once you have a set of clear financial goals it will be easier for you to assess your next action list.

- Start small and make it a habit. You don’t have to make it big at first. Always start with a small and doable amount.

Psych yourself and your wallet on saving 1000 pesos every month for example. At the end of the year you’ll have 12,000 pesos more on your savings fund.

Do not force yourself to save a lot of money at once, make it as gradual as possible so you won’t slack off midway.

- Join saving challenges. A good way to force yourself to save money each month is to join challenges. You can try the 52-Week Money Challenge, Invisible Money Challenge, 1% Money Challenge, and so on.

Increase your income. Our savings can be limited because of our income. Thus, try to increase your sources of income as much as possible. Engage yourself in extra income projects that you are passionate about. Choose a side hustle you can work on along with your full-time job.

Now where should you put your savings?

Cebuana Lhuillier Micro Savings is the perfect answer to the World Savings Day call to save more, especially for our fellow Filipinos who don’t have the means to really save.

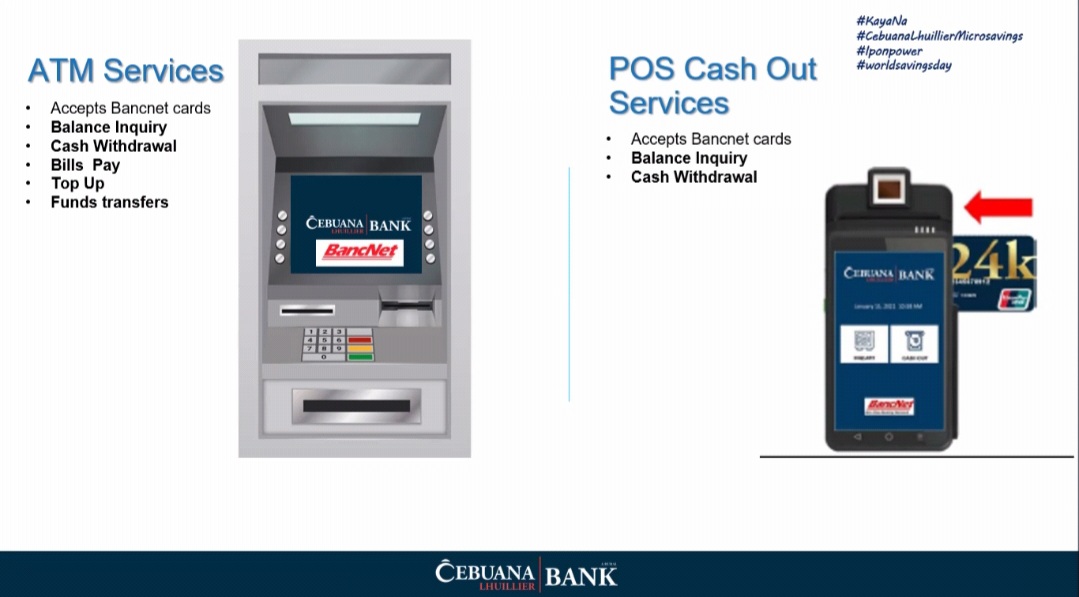

For one, the Cebuana Lhuillier Micro Savings account can be opened for only Php 50. Cebuana Lhuillier’s Micro Savings works like a normal savings account wherein you can deposit and withdraw anywhere at your most convenient time to Cebuana Lhuillier’s 2,500 branches nationwide.

Your Micro Savings account is already accredited to almost 21,000+ Bancnet ATMs nationwide for easy withdrawal. What’s amazing is you can even use your Micro Savings account to pay at any of 350,000 Unionpay and Bancnet accredited retail stores nationwide.

Last but not the least, Cebuana Lhuillier’s Micro Savings account offers a competitive interest rate of 0.20%. This is higher than other savings accounts can provide. And because there are zero to minimal fees whenever you do your transaction, your money will keep on growing. Just make sure you reach the minimum maintaining balance to earn interest which is Php 500.

{kind=link}